Governance Theatre: Starring DeFi

An odyssey of decentralization and its challenges

By Ellen Guo, Analyst @ e^{i} Ventures

Humans have always been engaged in a grand experiment with governance systems, in order to coordinate decisions affecting their collective future. Governance is a complex and difficult process underlying nearly all human endeavors. Today, decentralized finance is where millennia of human experience intersect with the speed and scale of internet communities, with the potent innovations of programmable money and trust-minimized transactions thrown into the mix.

Decentralized finance has revolutionized the crypto world in the past year, boasting nearly $82B in TVL at the time of this publication. DeFi applications are not only pursuing trustless and permissionless transactions but also decentralization of decision-making via governance. Instead of a centralized core team of trusted experts making decisions for the user community, the goal is to have changes determined directly by community participation and voting.

In my search for a deeper understanding of this newest chapter in humankind’s grand experiment, I surveyed the current state of decentralized governance to identify what’s working and what still needs work.

Background

Governance of a decentralized protocol refers to how the protocol’s various participants collectively make decisions about the protocol’s future. DeFi protocol participants are often rewarded with governance tokens when they perform actions that benefit the protocol. The amount of governance tokens held is typically correlated with the token-holder’s voting power. To date, most decentralized protocols follow the one token, one vote approach, in which each token entitles the token-holder a vote on community proposals. Proposals are generally aimed at modifying and upgrading the protocol.

Compound’s release of COMP in June 2020 initiated yield farming and a wave of DeFi governance. Since then, many other protocols have adopted a wide variety of novel approaches to governance.

Forms of Governance

DeFi protocol governance falls into two main paradigms: on-chain and off-chain.

On-chain Voting

Pioneered by Compound, on-chain governance systems conduct the entire proposal, voting, and implementation processes on the blockchain via smart contract interactions. The proposer calls the contract’s `propose` function with a list of executable commands, which run if the proposal passes. Voters interact with the smart contract directly to cast their votes. At the end of the voting period, votes are tallied and the proposal is either executed on-chain, or it fails.

Since on-chain voting requires proposals to be executable code, successful proposals can be implemented simply by executing the code. Results are secure and the integrity of the final count is protected by the robust security of on-chain consensus. However, submitting a proposal in on-chain governance systems requires a high degree of technical acumen. Also, depending on the underlying chain, proposers and voters may incur substantial transaction fees in order to participate.

Off-chain Voting

Off-chain governance systems allow users to submit proposals and vote without having to submit blockchain transactions. The most common off-chain voting platform, Snapshot, is open source software that stores proposals and votes as signed messages on IPFS. Snapshot gives protocol team members flexibility in creating their own spaces on Snapshot, including setting up rules that determine a token holder’s voting power.

Off-chain voting avoids transaction fees, which encourages broader community participation, but it requires a trusted third party to tally the votes. Additionally, implementation of successful proposals is not as simple as executing code. Proposals may require the core team or other representatives to take off-chain actions, such as writing new code or documentation, hiring someone, getting a legal opinion, or carrying out off-chain financial transactions.

Protocol Backgrounds

The differences in each protocol’s history and tokenomics can help in identifying what works well and what doesn’t.

Since governance is always evolving, data for this article is up to date until August 19, 2021.

Compound

Compound’s groundbreaking on-chain governance went live with the GovernorAlpha smart contract on April 16, 2020. After Proposal 42 (March 2021), the community migrated to GovernorBravo. Originally, any address with more than 100,000 COMP delegated to it could create proposals (i.e. calling the `propose` method). Proposal 52, executed July 14, 2021, lowered this threshold to 65,000 COMP. Proposals are passed by strict majority with a quorum of >400k COMP required.

Compound also implemented Compound Autonomous Proposals (CAPs) in September 2020 to lower the barrier for creating a proposal, since meeting the COMP threshold requires substantial financial resources (over $41 million at time of writing). Now anyone with 100 COMP can create a CAP, which are smart contracts that can have votes delegated to it by other community members. Once the required COMP threshold has been delegated to the CAP, it automatically launches an official, on-chain proposal.

Past Proposals

Total Proposals: 57

Executed: 48

Failed: 4

Cancelled: 4

In-progress: 1

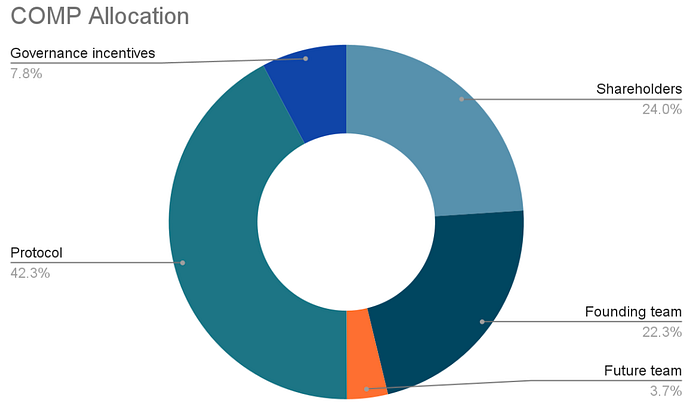

Tokenomics

Governance on Compound revolves around the COMP token, which is capped at 10,000,000. The initial distribution is:

The 2,226,037 COMP (22.3%) allocated to the founders and team are subject to 4-year vesting. Protocol COMP is released at the rate of 2,312 COMP/day, distributed to each market at a rate proportional to the interest accrued in each market (see current details here). Within each market, 50% goes to suppliers and 50% to buyers, with users earning COMP proportional to their balance.

Uniswap

Uniswap on-chain governance is a fork of Compound’s GovernorAlpha (though currently there is a proposal in progress to migrate to GovernorBravo), and functions essentially the same as Compound’s version. The proposal threshold was set to 10M UNI when governance was launched in September 2020, and was reduced to 2.5M with Proposal 4. The required quorum has always been 40M UNI.

In addition to on-chain proposing and voting, Uniswap encourages off-chain signalling prior to creating an on-chain proposal. You can see the specifics here, but in summary they specify a discussion forum and Snapshot Temperature Check (passes if majority and 25k UNI quorum), which graduates to a forum and Snapshot Consensus Check (passes if majority and 50k UNI quorum).

Past Proposals

Total on-chain proposals: 7

Executed: 3

Failed: 2 (both were quorum not reached)

Cancelled: 1

In progress: 1

Total off-chain proposals: 29

Passed: 18 (13 Temp Checks, 5 Consensus Checks)*

Failed: 11 (9 Temp Checks, 2 Consensus Checks)

* Assumes that unlabelled proposals are all Temperature Checks.

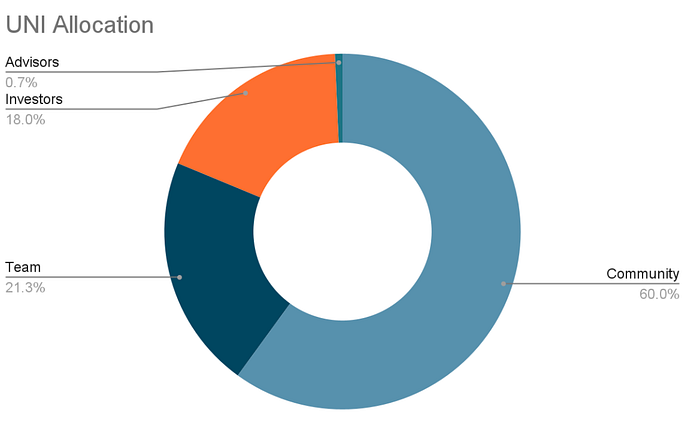

Tokenomics

When UNI went live September 16, 2020, 1 billion UNI were minted. The initial 4-year allocation is below. UNI dedicated to investors, current/future team members, and advisors are on a 4-year vesting schedule. Also inflation (2%/year) starts after 4 years.

At launch, a quarter of the 60% dedicated to the community (15%) was famously airdropped to wallets that had been liquidity providers, users, and SOCKS redeemers/holders. The governance treasury retained 43% to distribute to contributor grants, community initiatives, and liquidity mining This distribution is managed by community governance, and the last 2% of community UNI was released via liquidity mining in September-November 2020.

Sushiswap

Unlike Compound and Uniswap, Sushiswap’s governance is conducted exclusively off-chain, using Snapshot. Currently, only proposals posted by the Core team — 0xMaki (co-founder), Omakase (core dev), 0xJiro (core dev), or Ross Campbell (attorney) — are considered binding if passed with quorum (5M SUSHIPOWAH — see tokenomics). Once a “binding” proposal has passed, the Sushi team must implement the changes manually, though this is subject to the team’s availability.

As another safety check, any passed proposal that uses the devfund wallet requires approval by at least 6 of 9 signatories on the platform’s multisig (@SBF_Alameda, @rleshner, @0xMaki, @lawmaster, @cmsholdings, @mattysino, @mickhagen, @JiroOno, @zippoxer), and any ops changes, such as rebalancing and administration of farming pools, use of the growth fund, etc., requires at least 3 signatures from @0xMaki, @LevxApp, @OmakaseBar, @0xJiro, @0xKeno, @josephdelong, @MatthewLilley.

This structure of off-chain Snapshot votes (posted by core team members) and multi-sigs is only temporary, though. A 2021 roadmap indicates that Sushi aims to transition to a full-fledged DAO by Q4 2021.

Past Proposals

Total proposals: 243

Total core team proposals: 61*

*All future analysis of Sushiswap proposals only considers core team proposals. I also decided to exclude the multisig election proposals since the outcome is dependent across multiple proposals instead of the votes on just one proposal. For stats on the election, see this.

Tokenomics

Voting power is determined by SUSHIPOWAH balance. Each SUSHI in the SUSHI-ETH pool is worth 2 SUSHIPOWAH, and each SUSHI held via xSUSHI is worth 1 SUSHIPOWAH.

SUSHI supply is hard capped at 250M, and new SUSHI is created at 100 SUSHI/block for tokens staked in farms. Staking SUSHI returns xSUSHI and also earns 0.05% of the trade fee from all pools in the exchange.

Yearn

Yearn governance has evolved significantly since its inception. YFI was launched on July 17, 2020 with an on-chain governance architecture. Two proposals — Yearn Improvement Proposal (YIP) 1 and 12 — were passed before YIP-10 (July 24) was implemented and moved governance to a new smart contract due to security concerns. The new contract handled YIPs 30–45 before the community decided to move off-chain to Snapshot (archive Snapshot here, current Snapshot here) to avoid transaction fees and encourage higher community participation.

A notable feature of Yearn governance is its incentives to participate. YIP-45 gives a $500 yCRV bounty for proposing a YIP that reaches the “Implemented” phase, paid by the protocol’s treasury.

Past Proposals

Total proposals: 37

On first governance contract (on-chain): 7

Implemented: 3

Failed: 4

On updated governance contract (on-chain): 16

Implemented: 11

Passed: 12 (1 is waiting implementation)

Failed: 4

Off-chain: 15 (all passed, none implemented)

Tokenomics

YFI was launched on July 17, 2020, with 30,000 YFI minted. YFI is earned by providing liquidity to one of Yearn’s products, staking the output token in YFI distribution contracts, and earning a governance-controlled amount of YFI per day. On top of allowing governance votes, staking YFI earns a percentage of profits generated by Yearn.

Gemini considers the distribution a fair launch because no YFI was reserved for the founding team, investors, advisors, or other insiders.

An additional 6,666 YFI was minted as part of YIP-57 (⅓ to key contributors as vesting retention packages, and ⅔ to the Treasury).

Applied Governance

I measured four parameters to construct a view on how decentralized governance works in practice, then supplemented this with qualitative research on community engagement and discussion. The four parameters are voting power distribution, influential voters, authorship, and participation rates, and focused on the same sample set of DeFi protocols: Compound, Uniswap, Sushiswap, and Yearn.

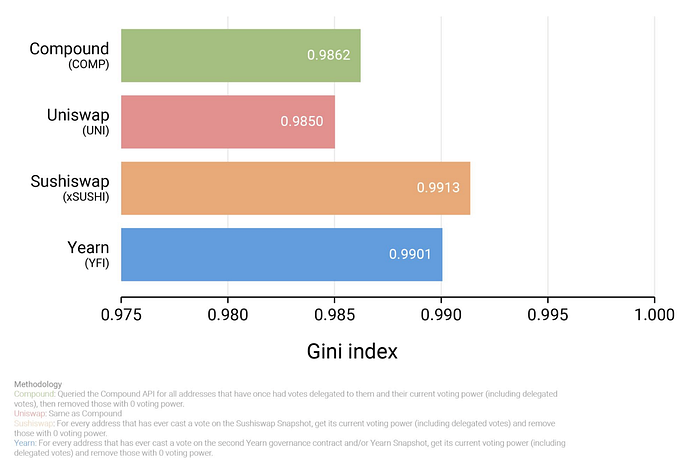

High Inequality of Voting Power Distribution

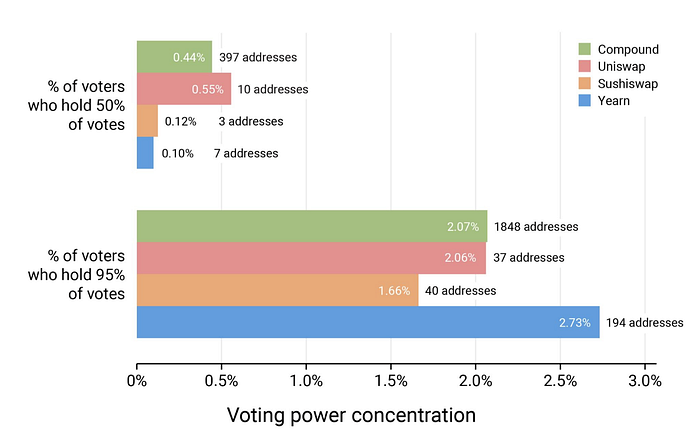

First, I looked at how voting power is distributed among the users of each protocol. Despite tokenomic differences, each of these protocols display high and comparable Gini coefficients, indicating a severe inequality in relative voting power of protocol users.

Less than 1% of voters in each of these protocols hold 50% of the delegated votes. Since voting is based on a strict majority, this means that <1% of voters could determine the outcome of every proposal in these protocols. The overwhelming majority of votes (95%) is held by <3% of voters across protocols.

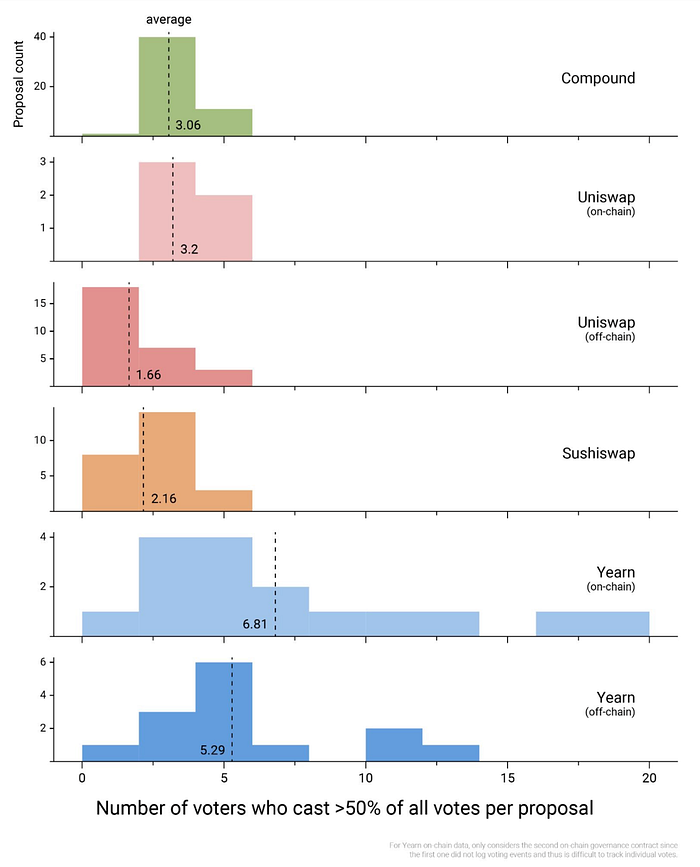

A Few Influential Voters Control Outcomes

The unequal distribution of voting power has a profound effect on the outcomes of proposals. For each proposal, I found the number of addresses that cast 50% or more of the total votes. Since the protocols considered here were based on a strict majority, these voters had the most influence over the outcome of each vote.

We can see that 2–7 voters are deciding the outcomes of nearly every proposal. Yearn’s governance (both on- and off-chain) exhibits a longer right tail in the distribution of the number of influential voters. In other words, the outcome of some proposals on Yearn are decided by more voters than in the other protocols. Despite this longer tail, on average 5–7 (and at most 20) Yearn voters are influencing the outcome of proposals.

Proposal Authors Tend to Be Core Team or Whales

Naturally, I then wondered, who’s submitting the proposals? I wanted to see how many addresses were proposing for each protocol.

Keep in mind, there are both technical and financial barriers to proposing. For the on-chain governances (Uniswap, Compound, and Yearn’s old system), writing and submitting a proposal requires technical background (call the governance contract’s `propose` function and write the executable functions in the proposal) and most protocols require the proposer to hold a minimum amount of that token to prevent low-quality, spammed proposals.

Compound’s threshold was 100,000 COMP ($ at time of writing) until mid-July, where Proposal 52 reduced the threshold to 65,000 COMP (~$43,700,000 at time of writing). However, with the introduction of Compound Autonomous Proposals, anyone with 100 COMP (~$43,700) can initiate the proposal process. Uniswap had a threshold of 10M UNI (~$260M) until mid-June, where Proposal 4 lowered the threshold to 2.5M UNI (~$65M); also, the fish.vote platform allows anyone with 400 UNI (~$10,400) can create an autonomous proposal. To create proposals on the Yearn Snapshot, you must hold at least 1 YFI (~$36,900); however, if your proposal has gained significant traction on the Discourse governance forum, Yearn team members will offer to propose it for you. As for Sushiswap, anyone can make a proposal on their Snapshot, but only those created by core team members are considered binding (i.e. will be implemented) once passed.

With this background, let’s investigate each protocol’s authors.

In general, we see that the majority of proposals are put forth by 3–7 addresses; much like the situation with the influential voters, authorship has been the product of a small circle.

For Compound’s 57 proposals, there were 17 unique proposers. The top 3 proposers were all large whales in the space: blck proposed 19, Geoffrey Hayes proposed 8, and Gauntlet proposed 7.

For Uniswap’s seven on-chain proposals, Dharma proposed the first two, the next two were autonomous proposals, and then once each by Harvard Law School Blockchain and Fintech Initiative, Dave Balter, and Getty Hill.

For Sushiswap, only the 4 core team members (as defined on the Snapshot) can create binding Sushiswap Snapshot votes.

For Yearn, each proposal also comes with a list of authors who were involved in drafting the proposal, not just the address that submitted the proposal. The authors are concentrated in the founding/core team as well: banteg (authored 9 proposals), lehnberg (8), milkylkim (8), tracheopteryx (8), Andre Cronje (6), Substreight (4), lex_node (4) — are all either members of the founding/dev/ops/legal team, or are currently/have been signers on the multisig.

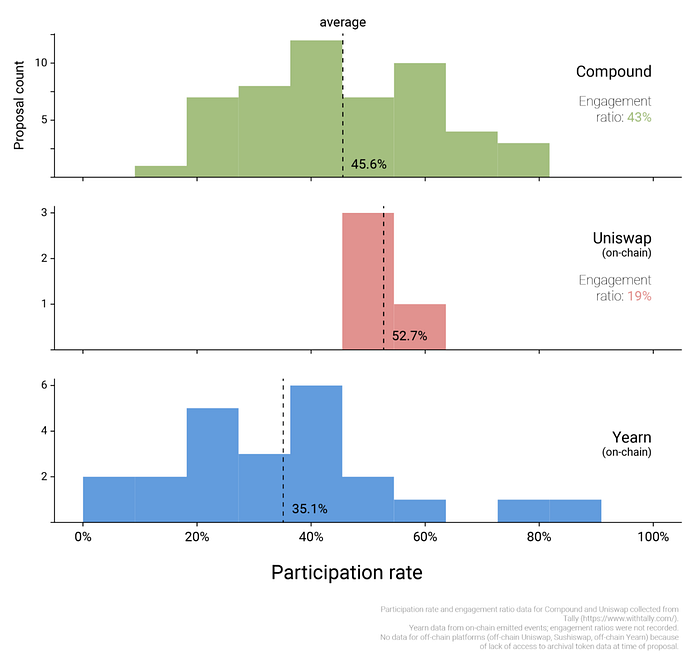

Voting Participation Rates Are Low

Once proposals are live, how does the community engage with them?

Statistically, there isn’t a significant difference between these distributions of participation rates, but the large spreads indicate that there are some proposals that garner notable participation while others are less active.

For Compound and Uniswap, this is the participation rate of delegated tokens (you must delegate your tokens before you can vote with them; you can delegate to yourself). The delegated tokens AKA engagement ratio based on total circulating tokens is 43% and 19%, respectively. In other words, on average, 43% * 45.6% = 19.6% of COMP tokens in circulation are being used in voting, and 19% * 52.7% = 10% for UNI.

However, I don’t think data analysis can capture the spirit and culture of decentralized governance, so I want to talk about two examples that have played out in DeFi governance recently.

Case Study: Uniswap DeFi Education Fund

Uniswap’s Proposal 5, to give 1M UNI to the DeFi Education Fund, has sparked controversy as an example of “governance theater.” Community members have criticized the lack of transparency — how so much money was given to a proposal that contained little detail as to what exactly would be done, how important questions raised by people like Chris Blec of DeFi Watch went unanswered, how though the proposal promised that 500,000 UNI would be liquidated over 4–5 years it was all sold in June. Yet the proposal passed due to the voting power of just a few addresses: mostly student groups (like the proposer, Harvard Law School Blockchain and Fintech Initiative), but all backed by a16z.

A user in the Uniswap Discord wrote, “I think this shows that the DAO and the treasury is at risk of centralized control if one organization and its allies can essentially write blank checks to themselves from the treasury.” In fact, discontent festered to the point of satire, where a proposal, mimicking the style of the Education Fund, was launched on the governance forum to create a fund to shave heads. Banteg, core dev at Yearn, wrote, “Despite the initial reaction to shrug it off as satire, I think this might be a good proposal to activate protest voters and shake up what’s essentially been a pretty dead governance token….You have my full support.”

Case Study: Sushiswap Phantom Troupe

On the Sushiswap governance forum, 0xMaki proposed to sell 51M SUSHI (at a discount) to institutional investors. Full coverage of how this situation — dubbed the Phantom Troupe — unfolded can be found in an article by DeFi Weekly here. TL;DR: “The community was outraged that a large portion of the treasury was being sold to investors who have no defined value add, at a large discount during all-time lows of $sushi with no clear reason for doing so.”

This outburst sparked more negotiations more favorable for Sushi, but eventually the proposal was entirely withdrawn. As Arca CIO wrote on the forum thread, “This is a case study in successful governance, and we’re thrilled to be a part of history, and the future, at the same time.” Or perhaps more powerfully, as DeFi Weekly wrote: “the power of the community has now risen to the point where they can openly negotiate with many institutional investors.”

The Path Forward for Decentralized Governance

Much of the data I collected seems to indicate that current DeFi governance is still in a transitional state and does not yet live up to the promise of trustless, permissionless community control; I find that voting power, influence, and authorship is concentrated in the hands of a few, with participation rates not reflective of broad community involvement. However, it’s important to note that decentralized governance is experimental and still in its infancy. Our findings support the intuitive conclusion that some degree of centralization is necessary during early formative stages with any project, as the community is still reaching critical mass, and the project is still establishing its relevance in the larger DeFi economy. DeFi governance is evolving rapidly through the use of both formal and informal technologies for coordination, all while trying to balance decision-making efficiency with decentralization.

Tokenomics

One of the loudest criticisms of DeFi governance is the unequal distributions of voting power, which centralizes power in the hands of a few. Though this is characteristic of early-stage DeFi governance, I think there’s more to the story.

Though the disparate token distribution structures across these protocols resulted in similar concentration of voting power, how voters perceive their votes seems to matter as well. For example, Yearn’s fair distribution might not have resulted in a substantially lower Gini, but it may cause voters to perceive that there aren’t large VCs or core team members dominating the vote; this hypothesis may explain why Yearn (both on- and off-chain) has a higher average number of influential voters.

Another aspect of tokenomics is distribution; perhaps why I’ve observed less community activity with Uniswap, compared to Sushiswap, is due to this. The only way users could have gotten UNI during the initial distribution is either through the retroactive airdrop or 3 months of liquidity mining (which still only counts for 17% of the total); all of the remaining UNI is either locked in the treasury or for the team/investors. This exclusive distribution may signal that getting involved is difficult and only for early movers, effectively excluding a large portion of users from governance. In contrast, SUSHI (and SUSHIPOWAH) is constantly emitted to users of the protocol.

Quadratic voting is one of the oft-suggested ideas for addressing unequal voting power distributions, and though it’s not within the scope of this article, I think it’s something that folks invested in governance should consider; Vitalik’s primer is a great start.

Proposal Authorship

Despite the apparent concentration of proposal authorship, it’s not unreasonable for voters to trust proposals written by well-known DeFi figures over those created by anon community members, especially when on-chain proposals require technical knowledge, or more importantly, implemented proposals can inflict substantial change to the protocol, for better or for worse. Secondly, most protocol leaders respect the governance forums, and official proposals (either on-chain or off-chain) generally reflect community opinion on the forums. In the Sushiswap Case Study, the negative community response meant that core team members did not propose a binding Snapshot vote.

I believe the introduction of autonomous proposals in Compound and Uniswap are promising mechanisms to encourage more decentralized authorship — even if a community member does not have sufficient tokens to propose something directly, as long as they garner enough community support, they’re still able to submit an on-chain proposal. Autonomous proposals are a way for smaller token-holders to feel heard which is crucial in decentralized governance: feeling heard directly impacts engagement and participation. As is true in traditional politics, when voters feel that their voices matter, they are more likely to vote.

If we take a look at Uniswap, after the introduction of fish.vote there were 2 autonomous proposals. It’s promising to see that the introduction of the autonomous proposals has democratized proposal authorship, but perhaps this is because the old proposal threshold (10M UNI) was incredibly high.

Additionally, through the reduction of the threshold to 2.5M UNI, I find that Dave Balter and Getty Hill held much less than the <10M UNI originally needed, indicating that the reduction has indeed allowed smaller players to propose as well. In other words, lowering proposal thresholds will allow more varied authors; of course, this may come at the expense of more spam-like proposals, though Yearn, with its lowest proposal threshold (1 YFI is about $36,900), has only had productive proposals.

In addition to autonomous proposals, robust governance forums seem to also facilitate healthy decentralized governance participation. Since anyone, regardless of token holdings, can comment and add ideas to proposal threads, forums are an incredibly powerful resource. However, it’s also incredibly important that official proposals reflect forum opinions; with the Uniswap case study, Harvard Law Blockchain disregarded the many concerns and complaints brought forward on the forum, which caused the community to lose trust in Uni governance and de-incentivized them from contributing to protocol governance.

Transparency

In my view, the most immediate and impactful improvement that DeFi projects can make to further their decentralization objectives is to lower barriers to community participation by improving governance documentation and transparency. When researching, I found that information could be hard to find or out of date. Questions about how the governance process works were a frequent topic in governance chat channels, especially from newer members of the community. In my view, protocols should focus their efforts on providing thorough and accessible documentation of governance processes, and help new members to get started with proposals, voting, or delegating their votes.

Closing

All in all, I’m very excited to see how DeFi governance continues to grow from here. What I love most about DeFi is how everyone can get involved to improve projects and the ecosystems at large. If you’re reading this, I bet you’re interested or invested in decentralized governance already. What do you think about DeFi governance? How do you think we can improve?

Brought to you by the team at e^{i} Ventures.

Written by Ellen Guo

Special thanks to: Nas, Srikar, Sol, Grace

Website: https://www.eiventures.io/

Twitter: https://twitter.com/eiventurestudio

Email: hello@eiventures.io

Disclaimer

The information provided by EI Ventures in this Medium Post pertaining to crypto-assets, business assets, strategy, and operations, is for general informational purposes only and is not a formal offer to sell or a solicitation of an offer to buy any securities, options, futures, or other derivatives related to securities in any jurisdiction and its content is not prescribed by securities laws.

Information contained in this Medium Post should not be relied upon as advice to buy or sell or hold such securities or as an offer to sell such securities. This Medium Post does not take into account nor does it provide any tax, legal or investment advice or opinion regarding the specific investment objectives or financial situation of any person. EI Ventures and its agents, advisors, directors, officers, employees and shareholders make no representation or warranties, expressed or implied, as to the accuracy of such information and EI Ventures expressly disclaims any and all liability that may be based on such information or errors or omissions thereof.

EI Ventures reserves the right to amend or replace the information contained herein, in part or entirely, at any time, and undertakes no obligation to provide the recipient with access to the amended information or to notify the recipient thereof.

The information contained in this Medium Post supersedes any prior Medium Post or conversation concerning the same, similar or related information. Any information, representations or statements not contained herein shall not be relied upon for any purpose.

Neither EI Ventures nor any of its representatives shall have any liability whatsoever, under contract, tort, trust or otherwise, to you or any person resulting from the use of the information in this Medium Post by you or any of your representatives or for omissions from the information in this Medium Post. Additionally, EI Ventures undertakes no obligation to comment on the expectations of, or statements made by, third parties in respect of the matters discussed in this Medium Post.